Duty free claims: Updated requirements for HTS Subheading 9801.00.10 – US and Foreign Goods Returned

The recent expansion of subheading 9801.00.10 of the Harmonized Tariff Schedule affects time limits for filing duty free claims for returned goods, and the documents that may be requested when reviewing such claims.

As discussed in US Customs’ CSMS #17-000046, subheading 9801.00.10 now includes all products exported from and returned to the United States, regardless of country of origin.

For US origin products, there is no time limit on filing a claim. For foreign origin products, there is a 3-year time limit. The provision affecting “Returned Property” applies to U.S. or foreign articles returned to the United States and entered or withdrawn from warehouse for consumption on or after April 25, 2016.

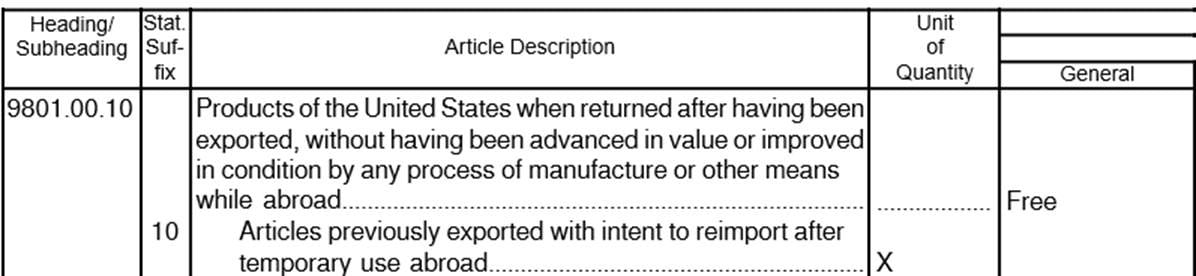

Previous language:

2017 language:

With respect to submission of documentation of duty free claims, CBP has outlined the specific types of written proof required when claiming duty free treatment under 9801.00.10. Prior to this clarification many were unclear as to what the requirement may be (e.g., Manufacturer’s Affidavit?, Form 3311?, Proof of export?)

- For either U.S. manufactured goods or foreign origin goods (for formal entries valued over $2,500 only): Declaration by Foreign Shipper indicating that the products were not advanced in value or condition while outside the United States. A certificate from the master of a vessel stating that the products are returned without having been un-laden from the exporting vessel may be accepted in lieu of the declaration by the foreign shipper;

- For U.S. manufactured goods (for formal entries valued over $2,500 only): for U.S. goods formally entered that are not clearly marked with the name and address of the U.S. manufacturer, CBP may require a Manufacturer’s Affidavit confirming that the articles were made in the United States;

- One of the following documents will be deemed sufficient proof of export from the United States for U.S. manufactured goods or foreign origin goods, provided the information contained therein proves an export from the United States:

- a) Copy of the entry into the foreign country;

- b) U.S. export invoice or bill of lading/airway bill; or)Electronic Export Information (EEI) or the Automated Export System (AES) filing exemption.

- For aircraft and aircraft parts and equipment returned to the United States by or for the account of an aircraft owner or operator and intended for use in his own aircraft operations, within or outside the United States, a CBP Form 3311, or its electronic equivalent may be used as stated in 19 CFR 10.1.

- For U.S. origin goods that were originally exported under a Department of State license that are now being re-imported, formal entry is required regardless of value along with the Directorate of Defense Trade Controls (DDTC) Partnership Government Agency (PGA) message set.

- For U.S. manufactured aircraft returning to the United States, that were sold to a foreign government under the Foreign Military Sales Program, formal entry is required if any maintenance is being performed on the aircraft while in the United States. The repairs have to be authorized via a specific case line in the Letter of Offer and Acceptance (LOA). The LOA is the agreement between the United States and the foreign government regarding the sale of munitions and other articles to the foreign government.

- a)At the time of export of the aircraft, the EEI has to be filed for the maintenance of the aircraft.

- For U.S. manufactured aircraft returning to the United States that were sold to a foreign government under the Foreign Military Sales program, where modifications or enhancements will be made to the aircraft, then the following is required for the import and subsequent export of the aircraft:

- a) Formal entry is required.

- b) At the time of export, the EEI submission is required, citing the Directorate of Defense Trade Controls export license (DSP-5).

ARRANGE YOUR CUSTOMSNOW ABI SOFTWARE WALK-THROUGH

Meet with a CustomsNow consultant to explore your compliance practices and how our best-in-class software and services can help you do what you do better.

CONTACT US